Fuel wise Electricity Generation Forecasts

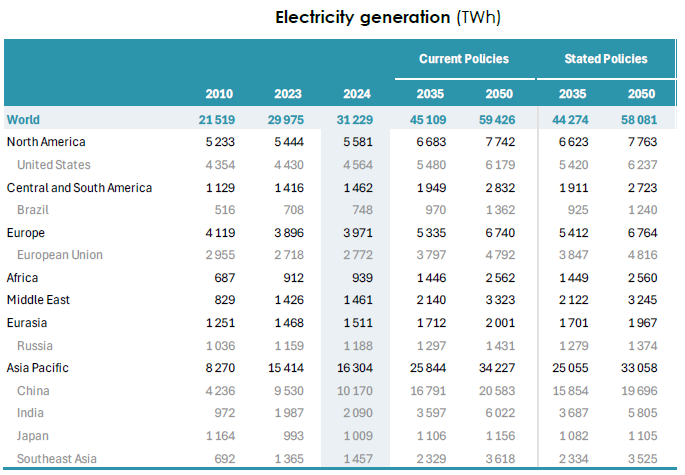

IEA expects world electricity generation to increase from 31,229 TWh in 2024 to 59,426 TWh and 58,081 TWh by 2050 in Current Policies and Stated Policies scenario respectively

IEA expects India’s electricity generation to increase from 2,090 TWh in 2024 to 6,022 TWh and 5,805 TWh by 2050 in the same two scenarios respectively

IEA expects China’s electricity generation to increase from 10,170 TWh in 2024 to 20,583 TWh and 19,696 TWh by 2050 in the same two scenarios respectively

Thus, India’s electricity generation is expected to almost match that of US by 2050, while China’s electricity generation is expected to be more than thrice that of US by that year

While there is not much difference in the quantum of total world electricity generation in the two scenarios, as discussed in subsequent paragraphs, the fuel-wise generation forecasts differ considerably under various scenarios

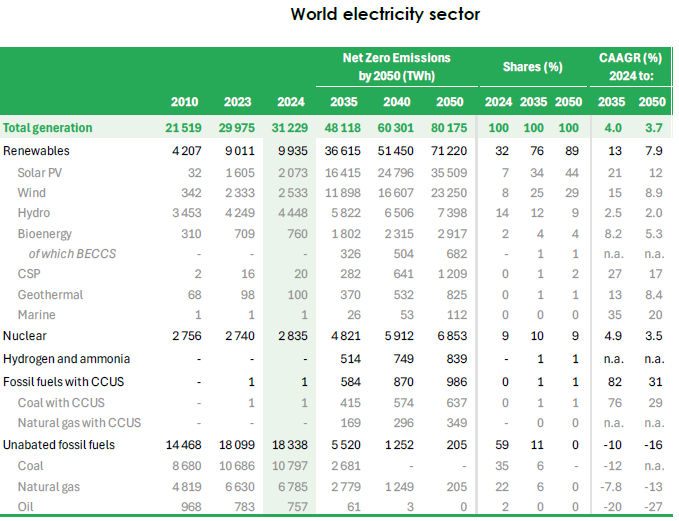

With progressively increasing requirement of electrification by low-carbon electricity in the Net Zero Emissions scenario, IEA expects world electricity generation to significantly increase from 31,229 TWh in 2024 to 80,175 TWh in this scenario

Renewables are expected to account for 71,220 TWh or 89% of total forecast electricity generation

BECCS (Bioenergy with Carbon Capture and Storage) generation produces energy (electricity, heat, biofuels) from biomass and then captures the resulting carbon dioxide for permanent underground storage, thus creating negative emissions. This is expected to play a small but important role due to these resultant negative emissions

There would be a marginal fossil fuels with CCUS generation, and even smaller unabated fossil fuels based generation

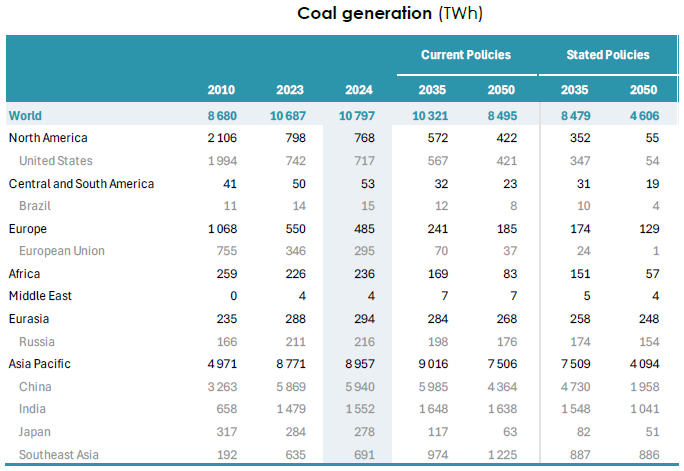

IEA expects world coal based generation to drop from 10,797 TWh in 2024 to 8,495 TWh and 4,606 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects India’s coal based generation to marginally increase from 1,552 TWh in 2024 to 1,638 TWh under Current Policies scenario, and decrease to 1,041 TWh in the Stated Policies scenario

IEA expects China’s coal based generation to decrease from 5,940 TWh in 2024 to 4,364 TWh and 1,958 TWh by 2050 in the two scenarios respectively

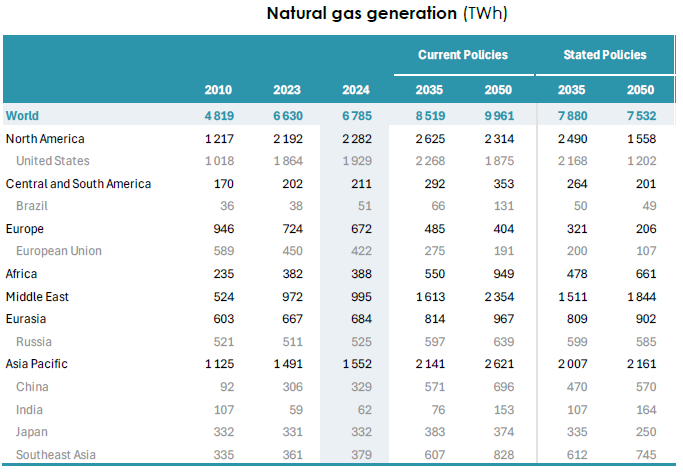

IEA expects world natural based generation to increase from 6,785 TWh in 2024 to 9,961 TWh and 7,532 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects India’s natural based generation to increase from 62 TWh in 2024 to 153 TWh and 164 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects China’s natural based generation to increase from 329 TWh in 2024 to 696 TWh and 570 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects world nuclear based generation to increase from 2,835 TWh in 2024 to 5,192 TWh and 5,531 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects India’s nuclear based generation to increase from 54 TWh in 2024 to 276 TWh and 337 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects China’s nuclear based generation to increase from 451 TWh in 2024 to 1,257 TWh and 1,408 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects US’ nuclear based generation to increase from 815 TWh in 2024 to 1,450 TWh and 1,573 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

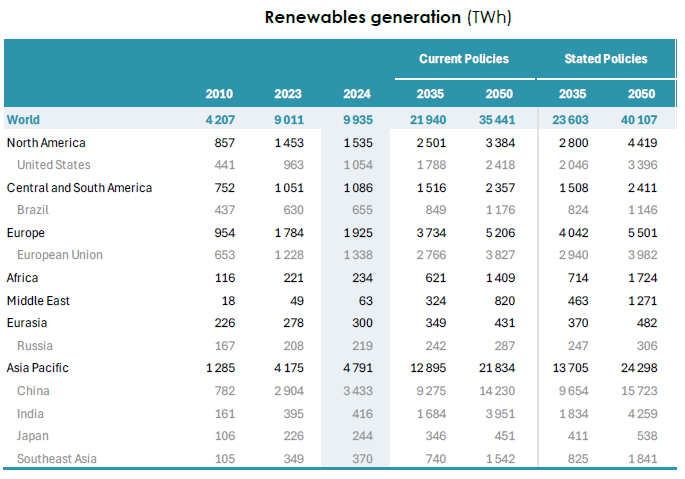

IEA expects world renewables generation to increase from 9,935 TWh in 2024 to 35,441 TWh and 40,107 TWh by 2050 in the Current Policies and Stated Policies scenario respectively. As covered in the Net Zero Emissions scenario in an earlier section, IEA expects world renewables generation to be 71,220 TWh by 2050 in this scenario, which is more than double the Current Policies scenario and 78% higher than in the Stated Policies scenario

IEA expects India’s renewables generation to increase from 416 TWh in 2024 to 3,951 TWh and 4,251 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects China’s renewables generation to increase from 3,433 TWh in 2024 to 14,230 TWh and 15,723 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

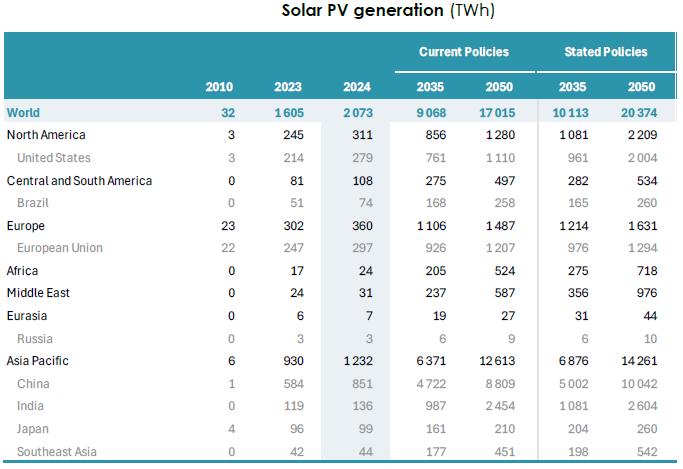

IEA expects world solar PV generation to increase from 2,073 TWh in 2024 to 17,015 TWh and 20,374 TWh by 2050 in the Current Policies and Stated Policies scenario respectively. As covered in the Net Zero Emissions scenario in an earlier section, IEA expects world solar PV generation to be 35,509 TWh by 2050 in this scenario, which is more than double the Current Policies scenario and 74% higher than in the Stated Policies scenario

IEA expects India’s solar PV generation to increase from 136 TWh in 2024 to 2,454 TWh and 2,604 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects China’s solar PV generation to increase from 851 TWh in 2024 to 8,809 TWh and 10,042 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

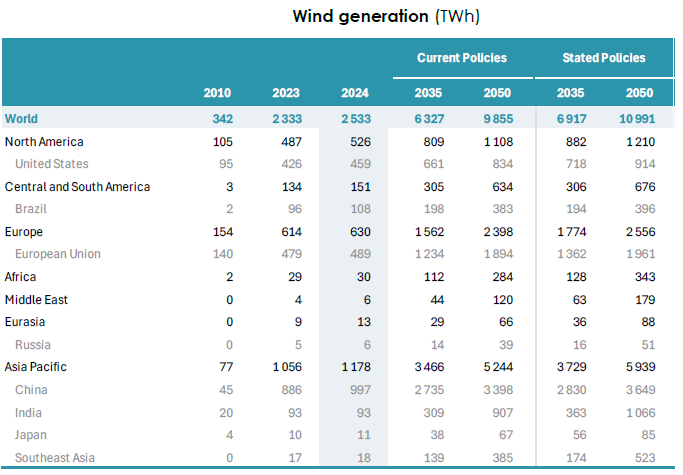

IEA expects world wind generation to increase from 2,533 TWh in 2024 to 9,855 TWh and 10,991 TWh by 2050 in the Current Policies and Stated Policies scenario respectively. As covered in the Net Zero Emissions scenario in an earlier section, IEA expects world wind generation to be 23,250 TWh by 2050 in this scenario, which is more than double the forecasts in both the Current Policies and Stated Policies scenarios

IEA expects India’s wind generation to increase from 93 TWh in 2024 to 907 TWh and 1,066 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

IEA expects China’s wind generation to increase from 997 TWh in 2024 to 3,398 TWh and 3,649 TWh by 2050 in the Current Policies and Stated Policies scenario respectively

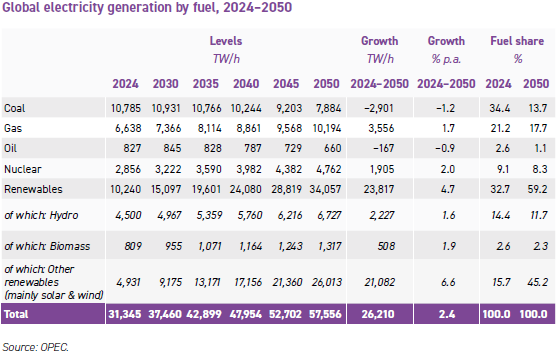

(Source: OPEC`s World Oil Outlook to 2050)

OPEC in its Outlook highlights that electricity demand has been increasing steadily since the beginning of the century, from around 15,500 TWh in 2000, global electricity demand soared to above 31,000 TWh in 2024. This is an increase of more than 100% since 2000, or around 3.15% p.a. on average. This was largely in line with global GDP growth over the same period, which increased at around 3.35% p.a. on average. Growing populations and economies were the main drivers of this power demand growth, coupled with increasing industrialization and rising middle classes

OPEC expects global electricity demand to increase from 31,345 TWh in 2024 to 57,556 TWh in 2050, an increase of nearly 85%. Around 75% of this growth is projected to come from developing countries, and almost 60% from developing countries in Asia alone. China is expected to see an increase of around 6,500 TWh in the outlook period, while India electricity demand is expected to grow by around 4,200 TWh

By far the largest increase in the generation mix is projected for other renewables (mostly wind and solar), which will grow from around 4,931 TWh in 2024 to 26,013 TWh in 2050, aided by energy policies and declining costs

Power generation from natural gas is projected to increase by 3,556 TWh between 2024 and 2050, in an effort to replace coal in the generation mix. Natural gas is a much cleaner fuel than coal, emits far less CO2 and reduces local air pollution significantly. Natural gas plants are also flexible and can begin operating within several minutes, ensuring they are well-suited to complement intermittent renewables and help balance their variability. Due to a strong expansion of intermittent renewables in some countries, it is possible that the operational regime for gas-fired plants will shift from baseload to peak load

Coal based generation is expected to fall from 10,785 TWh in 2024 to 7,884 TWh in 2050, or a decrease of 2,901 TWh