Liquids Supply Forecasts

(Source: OPEC`s World Oil Outlook to 2050)

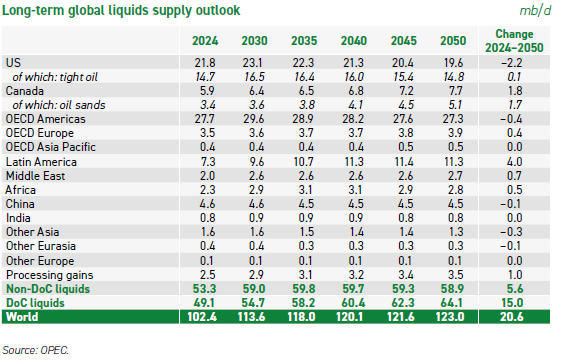

We briefly explain 2024 total liquids supply in the Table below :

Supply from OECD Americas was 27.7 mb/d, comprising 21.8mb/d from US and 5.9 mb/d from Canada

Non-DOC liquids supply was 53.3 mb/d, and DOC liquids supply was 49.1 mb/d, leading to total global liquids supply of 102.4 mb/d

DOC stands for Declaration of Cooperation. In late 2016, after months of talks, the Algiers Accord was signed by a group of OPEC and non-OPEC producers. The resulting DoC was agreed on 10 December of the same year. For the first time ever, OPEC Member Countries coordinated with a number of non-OPEC oil producing countries in a concerted effort to accelerate the stabilization of the global oil market

The Non-OPEC countries that are part of DOC are Azerbaijan, Bahrain, Brunei Darussalam (in 2016 Equatorial Guinea, which later joined OPEC), Kazakhstan, Malaysia, Mexico, Oman, Russian Federation Sudan and South Sudan

Hence DOC supply includes supply from OPEC members plus these Non-OPEC members which are part of DOC, whereas Non-DOC supply includes supply from all others including OECD Americas, OECD Europe, OECD Asia Pacific, Latin America, Middle East, Africa, China, India, Other Asia, Other Eurasia, Other Europe and Processing gains, and excludes DOC members belonging to these regions

OPEC expects total liquids supply to increase to 123 mb/d, comprising 58.9 mb/d Non-DOC liquids and 64.1 mb/d DOC liquids. Thus, Non-DOC liquids account for an increase of 5.6 mb/d and DOC liquids 15.0 mb/d of the total forecast growth of 20.6 mb/d

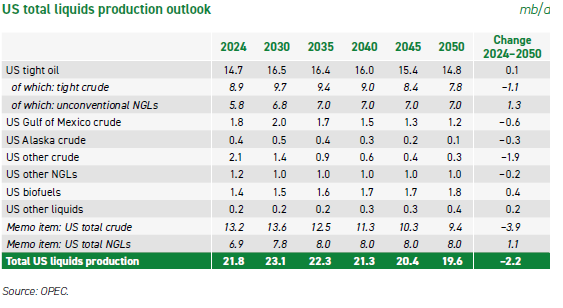

US deserves special attention in total liquids supply, with production at 21.8 mb/d in 2024 (13.2 mb/d crude oil + 6.9 mb/d NGLs + 1.4 mb/d biofuels and others)

On the 5-year forecast interval, OPEC expects US total liquids supply to peak at 23.1 mb/d in 2030, before slowly decreasing to 19.6 mb/d in 2050, as captured in the Table: