Discussion Paper on Compilation of Monetary Asset Accounts of Coal in India

24th June 2026

The Ministry of Statistics and Programme Implementation (MoSPI) has released a Discussion Paper titled `Methodological Approaches for Compilation of Monetary Asset Accounts of Coal in India`, aligned with the System of Environmental-Economic Accounting (SEEA) Central Framework, endorsed by the United Nations Statistical Commission as an international statistical standard

Since 2018, MoSPI has been following the UN SEEA Framework and compiling physical asset accounts for coal and other mineral and energy resources through the EnviStats India series and Energy Statistics India. Building on this foundation, MoSPI has taken a further step by initiating the experimental monetary valuation and compilation of monetary asset accounts for mineral and energy resources

The monetary valuation of environmental assets provides a measure of the economic value embodied in India's natural resource endowment, enables assessment of depletion costs, supports the estimation of future government revenues from resource extraction, and facilitates comparison across different environmental assets. The National Mineral Policy, 2019 mandates sustainable mining practices, making such valuation directly relevant to India's policy framework

About the Discussion Paper

The Discussion Paper presents a detailed conceptual framework for monetary valuation of non-renewable mineral and energy resources as prescribed in the SEEA Central Framework, and systematically reviews and compares three alternative international methodologies,OECD (2025) Compilation Guide for Measuring Natural Resources in the National Accounts,

the World Bank's Changing Wealth of Nations (CWON, 2024),

and the Philippines-based methodology (2024),

examining their conceptual foundations, data requirements, and potential data sources for the Indian context to identify the most appropriate approach for adoption within India's national statistical system

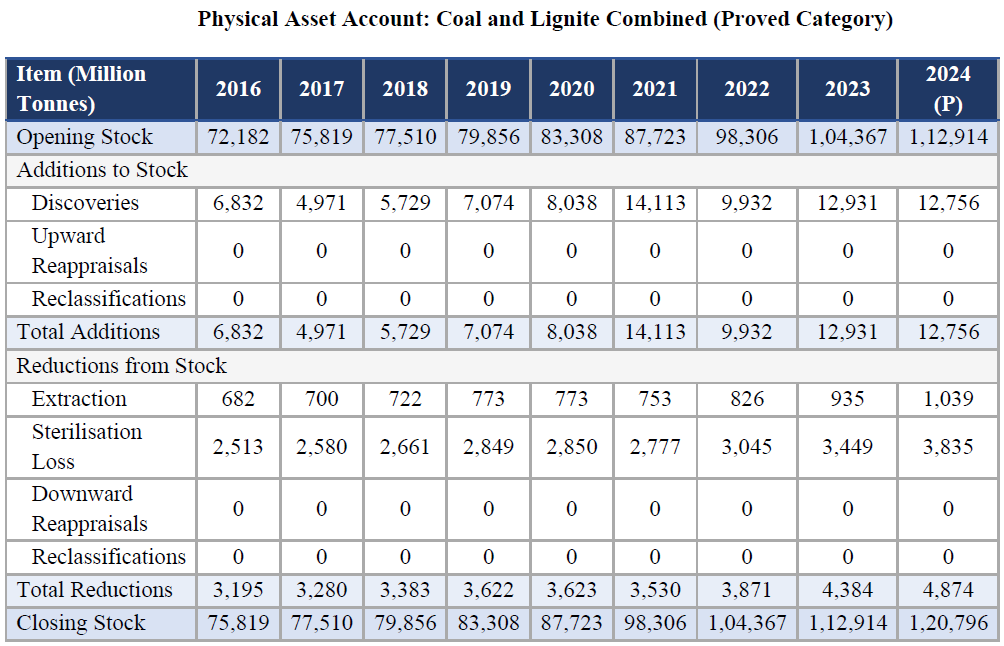

The paper also presents physical asset accounts for coal in India for the period 2015-16 to 2023-24, using data from the Geological Survey of India through EnviStats India 2024 and Energy Statistics India 2025

Coal has been selected as the illustrative case given its strategic importance to India's economy. As the nation's most abundant domestic energy resource, coal accounts for the majority of India's electricity generation and supports a wide range of core industries including steel, cement, and chemicals. India achieved record raw coal production of 1,047.523 million tonnes and lignite production of 45.133 million tonnes in 2024-25, underscoring the resource's centrality to India's energy security and the Atmanirbhar Bharat vision. At the same time, as a non-renewable resource, the need for its sustainable management makes monetary asset valuation all the more important

Key Findings and Recommended Methodology

Of the three methodologies reviewed, the OECD (2025) methodology is identified as the most appropriate for the Indian context, given its conceptual rigour, grounding in the SEEA Central Framework and the System of National Accounts (SNA 2025), and feasibility within India's existing data infrastructure, particularly the National Accounts Statistics (NAS) compiled by MoSPI. The methodology applies the Net Present Value (NPV) approach to future resource rents estimated through the Residual Value Method, drawing on national accounts aggregates This Discussion Paper is issued as an open invitation for comments and feedback from experts, researchers, government agencies, and international organisations. Responses received will assist in finalisation of a standardised methodology for monetary valuation of non-renewable mineral resources within India's national accounts framework, placing India at the forefront of natural capital accounting among emerging economies. Accurate and transparent monetary valuation of India's mineral and energy resources will serve as a foundational input for data-driven policymaking and sustainable developmentPhysical Asset Account: Coal and Lignite Combined (Proved Category)

Table below presents the physical asset accounts for coal in India for the period 2016 (2015-16) to 2024 (2023-24), compiled from EnviStats India 2024: Environment Accounts and Energy Statistics India 2025, MoSPI, aligned with the SEEA CF framework

The data for Coal and Lignite is obtained from the Geological Survey of India. Stocks and flows figures are sum of Coal (Proved) and Lignite (Proved) categories

Sterilisation Loss for Coal =Extraction*3.7 and for Lignite = Extraction*3.46 is applied, consistent with standard coal mining practice in India. Opening stock figures therefore reflect deductions for both extraction and sterilisation losses. Opening stock figures therefore reflect deductions for both extraction and sterilisation losses, and may differ from inventory data in the Coal Directory, which records geological resources without this adjustment (MoSPI, 2024)