K&A Analysis of India`s slot-wise Power Market on 25 April 2026

20th April 2026

Beyond the headline peak demand of ~256 GW, the real market story on 25 April 2026 lay in how strong solar generation during peak demand hours reduced dependence on fossil-fuel-based generation and kept DAM and GDAM prices softer. The sharper price signals emerged later in the evening, when solar generation declined and the call on coal and gas-based generation increased significantly

Our news item India Meets All-Time Highest Peak Power Demand of ~256 GW Without Shortage on 25th April 2026 at 15:38 hrs covered Ministry of Power's post

Here we present K&A Analysis of India’s slot-wise Power Market on 25 April 2026

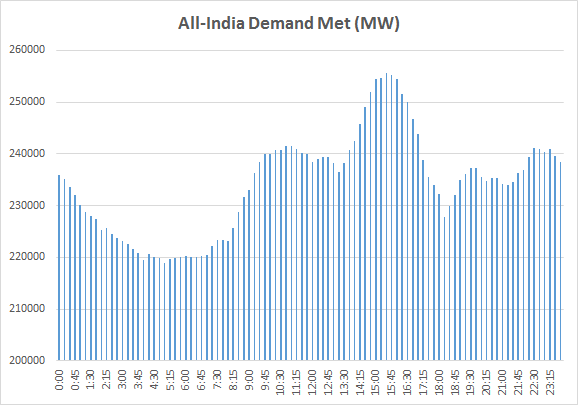

On 25 April 2026, India’s power system successfully managed an all-time high Demand Met of ~256 GW between the 15:30 to 15=45 blocks, without any reported shortage—an important operational milestone

Demand remained elevated through the day, varying from a minimum of 218,995 MW at 05:00 hours to the afternoon peak of 255,561 MW at 15:30 hours, reflecting strong summer demand conditions (The 256,117 MW peak demand occured at 15=38 hours, which is based on NLDC SCADA data)

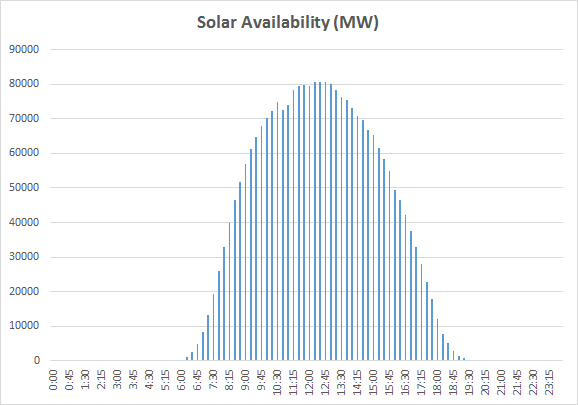

Solar generation played a crucial role in managing the system peak. Solar output rose from zero during night hours to a maximum of 80,801 MW at 12:30 hours, providing very strong support during the high-demand afternoon period

Importantly, the system peak at around 15:30 occurred while solar generation was still substantial, significantly reducing the burden on fossil-fuel-based generation. This demonstrates that a high peak demand does not necessarily translate into high power prices if peak demand aligns with strong solar availability

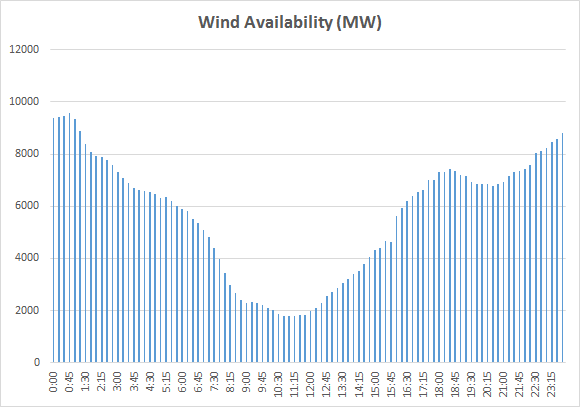

Wind generation, showed the usual contrasting pattern—highest during late night and early morning hours, with a maximum of 9,564 MW at 00:45 hours, but falling sharply to a minimum of just 1,776 MW at 11:15 hours, precisely when solar was strong

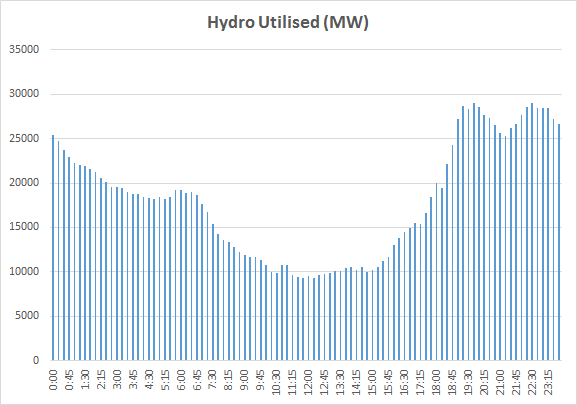

Hydro generation clearly served as the system’s balancing and peaking resource

Hydro output fell to a minimum of 9,299 MW at 12:15 hours, during peak solar hours when system stress was relatively low, and then rose sharply to a maximum of 29,012 MW at 19:45 hours, supporting the evening peak after solar withdrawal

This is a textbook example of hydro being optimally used as peaking power rather than as baseload generation

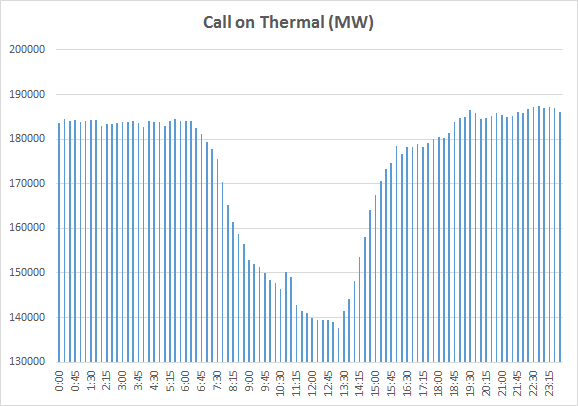

The combined call on Thermal + Gas—the best indicator of DAM and GDAM price setting, after renewable contribution—varied significantly across the day

It dropped to a minimum of 141,748 MW at 13:15 hours, when solar generation was near its strongest, and then rose sharply to a maximum of 196,801 MW at 22:45 hours, after solar generation had fully exited the system

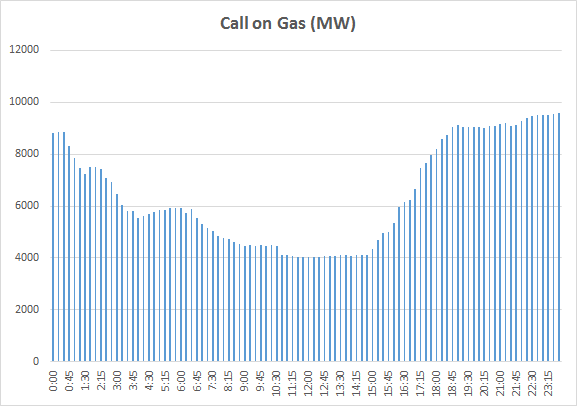

Coal Remained the Backbone; Gas Acted as the Marginal Balancer

Thermal generation (largely coal-based) remained the backbone of the system, varying from 137,656 MW at 13:15 hours to 187,306 MW at 22:45 hours

Gas generation—typically the highest-cost marginal source and often the strongest indicator for DAM price formation—varied from a minimum of 4,029 MW at 11:45 hours to a maximum of 9,565 MW at 23:45 hours

This doubling of gas dispatch strongly indicates that the system required expensive marginal balancing support during late evening and night hours, even though the absolute system demand peak had already passed

This is often where DAM prices are determined—not by peak demand alone, but by the timing of peak demand relative to renewable availability and the resulting call on gas generation

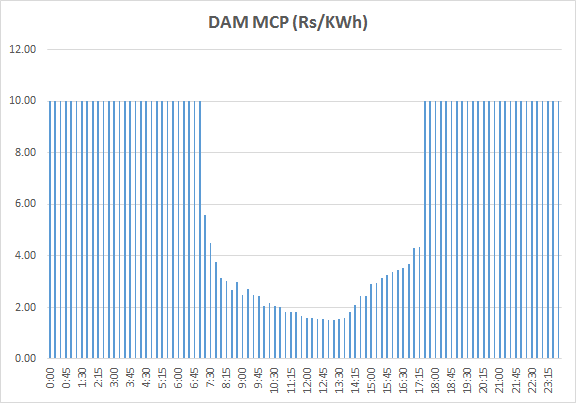

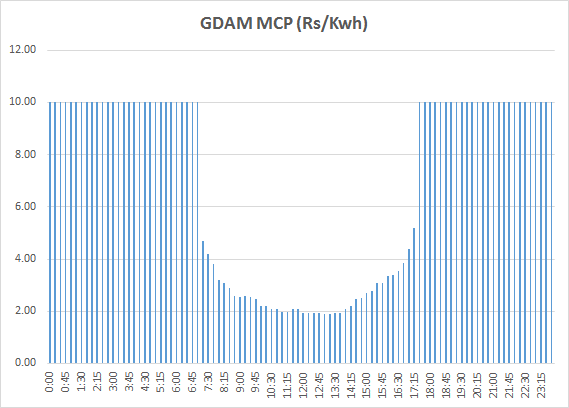

Despite very low prices during strong solar hours, both DAM and GDAM also witnessed prolonged periods at the regulatory ceiling price

DAM and GDAM prices remained soft during the afternoon solar window, when the call on Thermal + Gas was at its lowest. The Day Ahead Market (DAM) MCP touched its minimum of Rs 1.52/kWh at 13:00 hours, while the Green Day Ahead Market (GDAM) MCP reached its minimum of Rs 1.91/kWh at 13:15 hours—both closely aligned with the period of strongest solar contribution and the lowest residual fossil-fuel-based generation requirement

However, as solar generation tapered off and the system increasingly depended on fossil-fuel-based generation, prices strengthened sharply. Both DAM and GDAM hit the ceiling price of Rs 10/kWh in 55 out of the 96 time blocks, largely during evening, late-night, and early-morning hours when renewable support was limited and the call on Thermal + Gas was significantly higher

This clearly confirms that market prices were driven less by absolute peak demand and more by the timing of renewable withdrawal and the resulting dependence on higher-cost conventional generation, particularly gas

One of the most important policy implications—simple to understand but difficult to implement—is that India should progressively shift a larger share of its peak power demand into hours of maximum renewable generation, particularly strong solar hours

Imagine if this same peak demand of ~256 GW had occurred during evening hours after solar generation had exited the system—as is typically the case on many days across the year. The system would then have required an additional ~56 GW of fossil-fuel-based generation, significantly increasing dependence on coal and gas, and pushing DAM and GDAM prices much higher

This simple comparison highlights why the timing of peak demand matters as much as the magnitude of peak demand itself

This shift will not happen overnight. However, through sustained policy support, better demand-side management, time-of-day pricing signals, and consumer awareness, peak demand can gradually be aligned with renewable availability—reducing dependence on high-cost fossil-fuel-based generation and improving overall market efficiency

Having said that, no policy support by itself will achieve this goal. Generators, consumers, industries, regulators, market participants, and policymakers must consciously work together towards implementing this shift to capture the significant long-term benefits

When the entire ecosystem moves in that direction, the gains can be substantial—lower power costs, reduced dependence on high-cost fossil-fuel-based generation, improved market efficiency, and a stronger, more sustainable power system

Across days, months, and seasons, the exact numbers will change—but the underlying framework remains the same

Those who can identify future ₹10/kWh possibilities early, backed by robust slot-wise analysis rather than broad assumptions, and implement the right solutions quickly, are likely to be the winners in India’s evolving power market

These are precisely the windows where well-designed flexible resources—particularly Solar + Storage, demand response, flexible industrial loads, and fast-response peaking solutions—can create significant value by replacing high-cost fossil-fuel-based generation

As more participants enter and attempt to capture these high-price windows, both the duration of such high-price periods and the level of peak prices themselves can gradually reduce. However, given India’s expected rapid electricity demand growth, these premium-value hours will continue to exist—especially during evening ramps and seasonal peaks